Every year, thousands of French SMEs send transfers abroad without really knowing what they are paying for. Their bank shows an exchange rate, charges fees, and the transfer goes through. But behind this apparent simplicity lies a reality that is far more costly. SWIFT 2024 data have just confirmed it: the global interbank payment system processes hundreds of billions of dollars in transactions every day. And if you are among the businesses that regularly pay in foreign currencies, these figures concern you directly.

The dollar dominates: what this changes for your cash flow

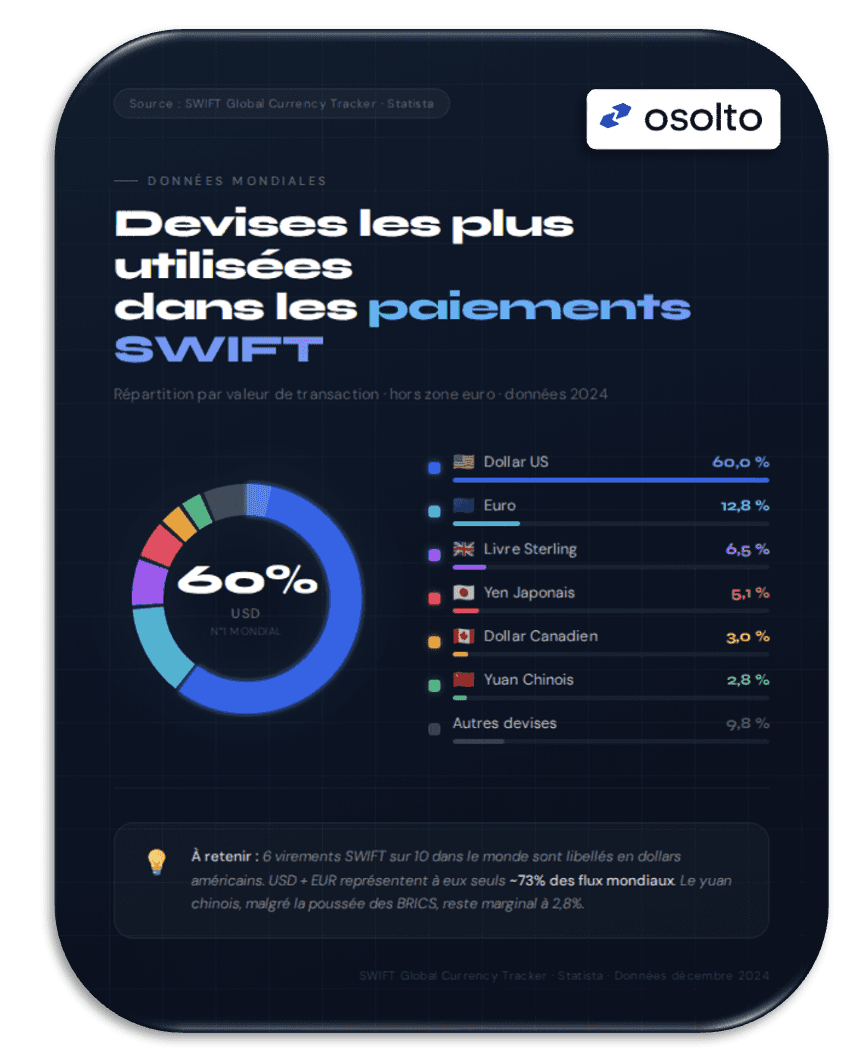

According to the SWIFT Global Currency Tracker (December 2024 data), 60% of international payments worldwide are denominated in US dollars. The euro follows at 12.8%, the pound sterling at 6.5%, and the Japanese yen at 5.1%.

Together, USD and EUR account for nearly 73% of all global flows.

What this means in practical terms: if your company pays suppliers in the United States, in Asia, or in any country whose local currency is pegged to the dollar, you are constantly exposed to EUR/USD fluctuations. And every exchange-rate movement has a direct impact on your margin.

What your bank does not tell you: the exchange rate it applies includes a commercial margin, generally between 1.5% and 3.5% above the real interbank rate. On a €50,000 transfer, that is between €750 and €1,750 that quietly disappears.

Chinese yuan at 2.8%: de-dollarisation, really?

Many media outlets talk about the rise of the yuan as an alternative to the dollar in global trade. SWIFT data puts a damper on that enthusiasm.

Despite the efforts of the BRICS countries and bilateral agreements in local currency, the yuan accounts for just 2.8% of global SWIFT payments. The Canadian dollar (3%) does even slightly better.

For your business, this means one simple thing: if you have flows to China, you are still paying overwhelmingly in USD or EUR — with all the currency-conversion constraints that entails.

Why these figures should change the way you manage your payments

The concentration of flows in a handful of currencies creates two risks that many business leaders underestimate.

Exchange-rate risk first. When 60% of global transactions are conducted in dollars, any European company that buys or sells in USD is exposed to EUR/USD volatility. In 2022, that pair lost nearly 15% in a few months. For an SME making €500,000 of annual payments in dollars, the impact can exceed €50,000 in unanticipated losses.

The risk of banking mark-ups, then. The more a currency is used, the more traditional banks know they can apply comfortable margins without their clients questioning them. The dollar and the euro are the first victims of this phenomenon.

How to reduce your SWIFT payment costs immediately

The good news: there are now regulated alternatives to traditional banking channels for your international payments.

At OSolto, an ORIAS-approved payment intermediary supervised by the ACPR, we support French SMEs across all their foreign-currency flows — whether one-off transfers or recurring payments to overseas suppliers.

Our approach is simple: access to the real interbank exchange rate, fixed and transparent fees per transaction, with no account maintenance fees. Result: our clients immediately recover up to 50% on their exchange costs compared with their usual bank.

And because every flow is different — amount, currency, schedule, frequency — every analysis is personalised and free.

Conclusion

The SWIFT 2024 data is clear: the dollar remains king of international payments, and European companies remain massively exposed to exchange costs. That does not have to be inevitable.

An analysis of your flows takes less than 30 minutes and can reveal significant savings from the very first transfer.

→ Get your free analysis on osolto.com

FAQ

What is the SWIFT network? SWIFT (Society for Worldwide Interbank Financial Telecommunication) is the interbank messaging system used by more than 11,000 financial institutions worldwide to make international payments.

Why does the dollar dominate SWIFT payments? The dollar has been the world's reserve currency since the Bretton Woods agreements (1944). The majority of commodities, oil, and international commercial contracts are denominated in USD, which mechanically creates massive demand.

How can I reduce fees on my SWIFT transfers? By using a regulated payment intermediary like OSolto, you access the real interbank rate instead of your bank's marked-up rate, and pay fixed transparent fees rather than a percentage of the amount.

Is OSolto regulated? Yes. OSolto is registered with ORIAS and supervised by the ACPR, the French regulatory authority for payment service providers.